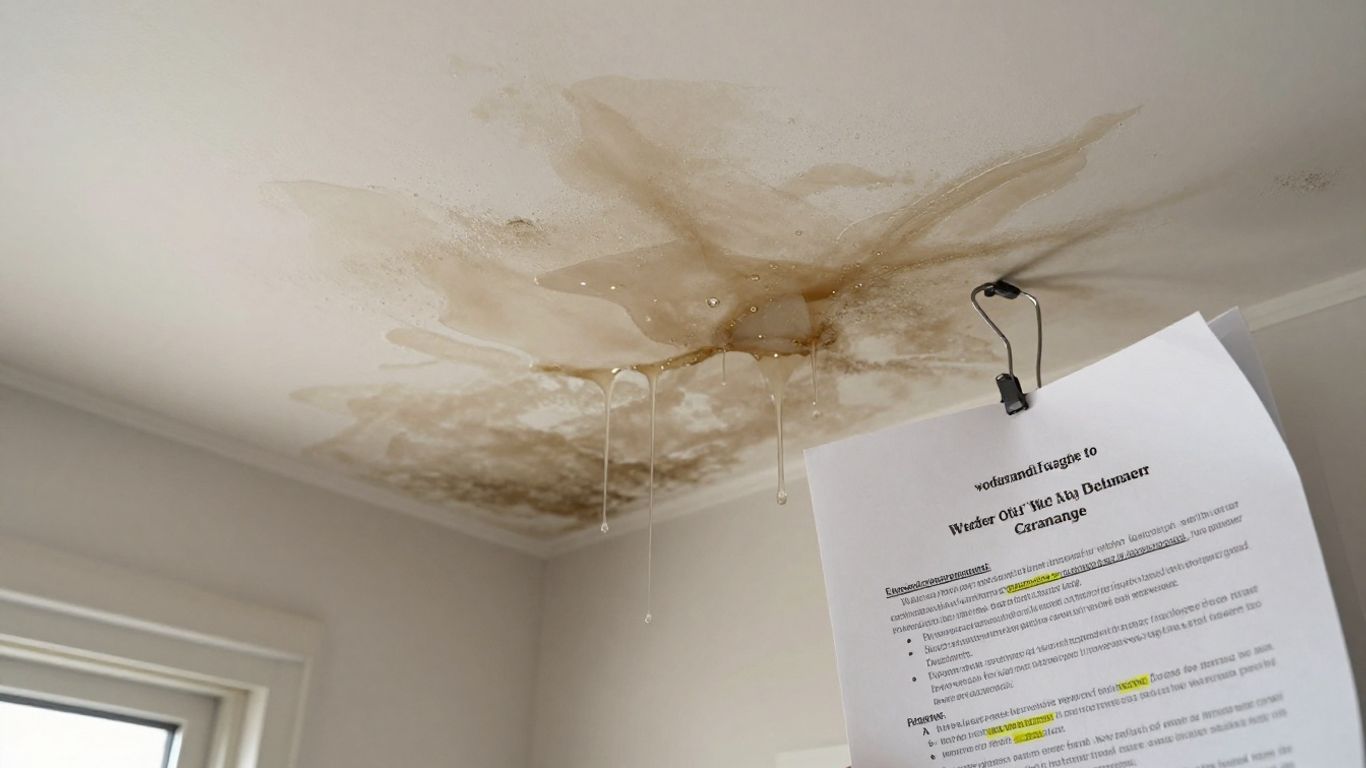

Water is a big deal in our lives, but not when it’s showing up where it shouldn’t be, like in your living room. Water damage is a super common reason people file claims on their home insurance. It can happen from all sorts of things, and knowing what your policy actually covers can save you a lot of headaches and money down the road. So, will homeowners insurance cover water damage? Let’s break it down.

Key Takeaways

- Standard homeowners insurance usually covers water damage if it’s sudden and accidental, like from a burst pipe or a leak during a storm. It generally doesn’t cover damage that happens slowly over time due to poor maintenance.

- The source of the water is important. Damage from inside your home (like a broken pipe) is often covered, but damage from outside sources (like flooding from a river) usually isn’t and requires separate flood insurance.

- Things like sewer backups and drain overflows aren’t typically covered by a basic policy. You can usually add this protection with an endorsement or separate policy.

- Your policy covers the damage to your home and belongings, but often not the item that caused the leak or overflow itself, like a faulty appliance. That’s usually considered wear and tear.

- If water damage makes your home unlivable, your policy might cover additional living expenses, such as hotel stays and meals, while repairs are being made.

Understanding What Triggers Water Damage Coverage

When water decides to make an unwelcome appearance in your home, the first question on your mind is probably, "Will my insurance cover this?" It’s not always a simple yes or no. The key to figuring out coverage often comes down to understanding where the water came from and how it got there. Insurance companies look at a few main things to decide if a water damage claim is covered.

The Source of Water Intrusion Matters

Think of it like this: water coming from inside your house is generally viewed differently than water coming from outside. A burst pipe in your living room? That’s usually a different story than a river overflowing its banks and flooding your basement. Standard homeowners policies are typically designed to handle sudden, accidental issues originating within the home’s systems.

Sudden and Accidental vs. Gradual Damage

This is a big one. Insurance policies usually cover damage that is sudden and accidental. This means something unexpected happened quickly, like a pipe freezing and bursting during a cold snap, or your washing machine hose breaking and flooding the laundry room. These events are generally unpredictable and happen fast.

On the flip side, damage that happens slowly over time, often due to lack of maintenance or just general wear and tear, is usually not covered. This includes things like a slow drip from a faucet that you never got around to fixing, or water seeping into your basement through foundation cracks over months or years. Insurers often see this as preventable damage. It’s important to address small issues before they become big, costly problems. For instance, slow seepage can lead to mold issues over time, and while mold from a sudden covered event might be addressed, mold from ongoing moisture is often excluded. Understanding mold remediation costs can be complex, so knowing your policy is key.

The Role of Maintenance and Neglect

Your insurance policy is there to protect you from the unexpected, not necessarily from the consequences of not taking care of your home. If damage occurs because of poor maintenance or neglect, your claim might be denied. This could mean not fixing a known leaky roof, ignoring signs of seepage around your foundation, or not maintaining your plumbing system. The idea is that homeowners are expected to take reasonable steps to maintain their property. If you’ve been neglecting obvious issues, the insurance company might argue that the damage was preventable and therefore not covered.

Here’s a quick breakdown:

- Covered: Sudden pipe bursts, appliance overflows, damage from firefighting efforts.

- Likely Not Covered: Slow leaks, flood damage from external sources, sewer backups (without add-on coverage), damage from long-term neglect.

- Depends on Policy: Water backup and sump pump issues often require specific endorsements.

It’s always a good idea to review your policy documents or speak with your insurance agent. They can clarify what specific events and types of water damage your particular policy covers and what it excludes. Don’t wait until disaster strikes to find out!

Remember, even if the damage itself is covered, the policy usually won’t pay to fix the item that caused the leak, like the faulty appliance or the old pipe. It covers the resulting damage to your home and belongings.

Key Factors Determining Coverage for Water Damage

When water decides to make an unwelcome appearance in your home, figuring out if your insurance policy has your back can feel like a puzzle. It’s not always a simple yes or no. Several things play a big role in whether a water damage claim gets approved. The specifics of your policy and the exact circumstances of the damage are what insurance companies look at most closely.

Identifying the Cause of the Water Damage

This is probably the biggest factor. Where did the water come from, and how did it get there? Insurance policies tend to look favorably on water damage that happens suddenly and unexpectedly. Think of a pipe that bursts out of nowhere during a cold snap, or a washing machine hose that suddenly gives way. These are usually covered because they’re seen as accidents.

However, if the water damage is the result of something that’s been happening over a long time, or something you could have reasonably prevented, you might be out of luck. This includes things like:

- Slow leaks from aging pipes that you didn’t fix.

- Water seeping in through cracks in your foundation over years.

- Mold or mildew that grew because a small leak was ignored.

Basically, if it looks like neglect or just the natural aging of your home, insurers are less likely to cover it. They want to see that you’ve taken reasonable steps to maintain your property.

Distinguishing Between Policy Types

Not all homeowners insurance policies are created equal, and this is especially true when it comes to water damage. A standard policy might cover a burst pipe, but it probably won’t cover damage from a flood. You need to know what kind of policy you have and what it includes.

- Standard Homeowners Policy: Typically covers damage from internal sources like burst pipes, appliance overflows, and leaks from a sudden roof damage event.

- Flood Insurance: This is a separate policy, usually needed if your home is in a flood zone. It covers damage from rising water, storm surge, and overflowing bodies of water.

- Water Backup and Sump Pump Coverage: This is often an add-on to your standard policy. It’s for those unfortunate events where water or sewage backs up into your home from outside drains or if your sump pump fails.

It’s a good idea to review your policy documents or chat with your insurance agent to make sure you understand the boundaries of your coverage. You might be surprised by what’s included and, more importantly, what’s not.

The Importance of Policy Exclusions

Every insurance policy has a section detailing what is not covered. These are called exclusions, and they are super important to understand. For water damage, common exclusions often include:

- Damage from floods (unless you have separate flood insurance).

- Sewer or drain backups (unless you have specific water backup coverage).

- Damage from gradual leaks, seepage, or general wear and tear.

- Mold or mildew that results from long-term moisture issues.

Understanding these exclusions upfront can save you a lot of heartache and money down the road. It helps set realistic expectations about what your insurance will and won’t pay for when water damage strikes. Don’t just assume; actively look for these details in your policy.

Sometimes, even if the cause seems covered, an exclusion might still apply. For instance, if a pipe burst but the insurer can prove it was due to lack of maintenance, they might deny the claim based on an exclusion related to neglect. It’s always best to be proactive about home maintenance to avoid falling into these coverage gaps. If you’re concerned about mold from persistent moisture, looking into mold remediation services might be a good idea, but remember that insurance usually covers the cause of the damage, not necessarily the cleanup of the resulting mold if it’s due to long-term issues.

Common Water Damage Scenarios Covered by Insurance

Water damage is a real headache, and it’s one of the most frequent claims homeowners make. When water decides to make an unwelcome appearance in your home, knowing what your insurance policy might cover can save you a lot of stress and money. Generally, standard homeowners insurance is designed to help with water damage that is sudden and accidental. Think of it as protection against unexpected events, not ongoing issues that could have been prevented with a little upkeep.

Burst Pipes and Plumbing Leaks

This is a big one. If a pipe suddenly bursts due to freezing temperatures or just decides to give up the ghost, the resulting water damage is usually covered. This includes leaks from supply lines, interior pipes, or even an overflowing toilet or sink that wasn’t caused by neglect. The key here is that the event was unexpected and happened quickly. So, if a pipe ruptures and floods your kitchen, your policy will likely help pay for the repairs to your flooring, cabinets, and walls, up to your policy limits. It’s also good to know that damage caused by firefighting efforts, like water from hoses used to put out a fire, is typically covered too.

Appliance Malfunctions and Overflows

We rely on our appliances daily, but sometimes they fail. If your washing machine hose splits, your water heater springs a leak, or your dishwasher overflows, the water damage to your home itself is often covered. Your policy might help repair the floors, walls, or cabinets that got soaked. However, it’s important to remember that the appliance that caused the problem usually isn’t covered by homeowners insurance. That’s typically considered wear and tear, and you might need a separate home warranty for that.

Damage from Firefighting Efforts

It might seem counterintuitive, but when firefighters battle a blaze at your home, the water they use to extinguish the fire can cause significant damage. Fortunately, homeowners insurance policies generally cover water damage that results from these firefighting efforts. This means if the water used to put out a fire damages your home’s structure or your belongings, your policy should help with the costs of repair or replacement.

Roof Leaks from Sudden Storms

When a severe storm hits, and wind or hail damages your roof, allowing rain to come in, that’s usually a covered event. If a tree falls on your roof during a storm, or high winds rip off shingles, and water then enters your home, your policy will likely cover the resulting water damage. This protection applies to the damage caused by the storm itself and the water that gets in because of that sudden damage. It’s a good idea to check your roof regularly, especially after major weather events, to catch any potential issues early. If you live in an area prone to severe weather, you might want to look into flood insurance options, as standard policies often exclude damage from rising water.

It’s always a good idea to review your policy documents with your insurance agent. They can help clarify what’s covered and what’s not, especially when it comes to specific scenarios like appliance failures or roof leaks. Understanding the details can prevent surprises down the line.

Here’s a quick rundown of common covered scenarios:

- Burst pipes: Frozen pipes, old pipes that fail suddenly.

- Appliance leaks: Washing machines, dishwashers, water heaters.

- Overflows: Toilets, sinks, tubs (if not due to long-term neglect).

- Storm damage: Rain or snow entering due to sudden roof or wall damage.

- Firefighting water: Water used by emergency services to put out a fire.

Water Damage Situations Typically Not Covered

So, you’ve got water damage. Bummer. While your homeowners policy is a lifesaver for many things, it’s not a magic wand for every single water-related mishap. Some situations just aren’t on the typical policy’s radar, and it’s good to know what those are before you need to file a claim.

Flood Damage from External Water Sources

This is a big one. If water comes into your home from the outside – think heavy rain, overflowing rivers, storm surge, or even just surface water runoff pooling around your foundation – that’s usually considered flood damage. Standard homeowners insurance policies generally don’t cover this. You’ll likely need a separate flood insurance policy for that kind of protection, especially if you live in an area prone to flooding.

Sewer and Drain Backups

Another common exclusion is damage from sewer or drain backups. If your pipes back up and sewage or water starts coming into your home from the municipal sewer system or even your own drain lines, your standard policy probably won’t foot the bill. This is a pretty common issue, and thankfully, most insurers offer an add-on coverage for water and sewer backups. It’s usually not too expensive and can save you a lot of headaches.

Gradual Leaks and Seepage

This is where things get a bit tricky. Insurance is generally designed to cover sudden, accidental events, not slow, creeping problems. If you have a leaky faucet that’s been dripping for months, a slow seep from your foundation, or water gradually getting in through old roof shingles, that’s usually considered gradual damage. Insurers often see these as maintenance issues that could have been addressed before they caused significant harm. The key here is that if the damage develops over time due to lack of upkeep, it’s often not covered.

Damage from Wear and Tear

Similar to gradual leaks, damage that happens simply because your home is aging or because things are worn out isn’t typically covered. This includes things like old, corroded pipes finally giving way or water damage resulting from the natural breakdown of materials over time. Your policy isn’t meant to be a perpetual maintenance plan for your home; it’s there for unexpected disasters. So, while your policy might cover the water damage from a burst pipe, it probably won’t pay to replace the old pipe itself.

It’s really important to remember that "gradual" damage is the opposite of what most policies are designed to cover. Think of it like this: if you could have reasonably seen this coming and done something about it, the insurance company likely won’t cover the resulting mess.

How Your Homeowners Policy Protects Against Water Damage

When water decides to make an unwelcome appearance in your home, your homeowners insurance policy is designed to step in and help. It’s not just about the big floods; even smaller, unexpected water issues can cause a lot of damage, and your policy has different parts to cover various aspects of that. The main goal is to help you repair your home and replace damaged belongings so you can get back to normal.

Dwelling and Other Structures Coverage

This part of your policy, often called Coverage A, is for the actual house itself. If a pipe bursts inside your wall and causes damage to the drywall, flooring, or even the framing, this coverage helps pay for those repairs. It’s not just the main house, either. If you have a detached garage, a shed, or a fence that gets damaged by a covered water event, Coverage B (Other Structures) would kick in to help fix those too.

Personal Property Protection

Beyond the structure of your home, your stuff inside it matters too. Coverage C, or Personal Property Protection, is there to help you replace or repair items that get damaged by water. Think furniture, electronics, clothing, and other belongings. It’s important to know that there might be limits on certain high-value items, so it’s a good idea to check your policy details. Making a detailed home inventory can be super helpful here, especially if you need to file a claim.

Additional Living Expenses Coverage

Sometimes, water damage is so bad that you can’t live in your home while it’s being repaired. That’s where Additional Living Expenses (ALE), or Coverage D, comes in. This coverage helps pay for the extra costs you incur if you have to temporarily move out. This could include hotel stays, restaurant meals if you can’t cook, laundry services, and other necessary expenses. It’s meant to cover the difference between your normal living expenses and what you have to spend while your home is being fixed.

It’s really about getting you back on your feet. Your policy is structured to cover the physical damage to your house and property, and also the costs associated with being displaced. The key is that the water damage itself must stem from a covered event, like a sudden pipe burst, not something that’s been happening for ages due to neglect.

Here’s a quick look at what these coverages generally address:

- Dwelling Coverage (Coverage A): Repairs to the main house structure (walls, roof, floors).

- Other Structures Coverage (Coverage B): Repairs to detached structures like garages or sheds.

- Personal Property (Coverage C): Replacement or repair of damaged belongings (furniture, electronics, etc.).

- Additional Living Expenses (Coverage D): Costs for temporary housing and related expenses if your home is uninhabitable.

Optional Coverages for Enhanced Water Damage Protection

So, your standard homeowners policy has some gaps when it comes to water damage. That’s pretty common, honestly. Water is sneaky, and sometimes the damage it causes isn’t covered by the basic plan. Luckily, there are ways to beef up your protection. Think of these as add-ons, like getting extra cheese on your pizza – it just makes things better when the unexpected happens.

Adding Flood Insurance

This is a big one. If you live anywhere near a river, a coast, or even just an area that gets a lot of rain, your standard policy probably won’t cover damage from rising water. That’s where flood insurance comes in. It’s a separate policy, and it’s specifically designed to cover damage from external water sources like overflowing lakes, storm surges, or even just heavy rainfall that can’t drain properly. It’s a really smart move if you’re in a flood zone or even just a moderate-risk area. You can get this through the National Flood Insurance Program or private insurers. It’s not usually included in your regular home insurance, so you have to ask for it specifically.

Securing Water Backup and Sump Pump Coverage

This is another common area where standard policies fall short. What happens if your sewer backs up into your basement? Or if your sump pump fails during a heavy rain and your basement floods? Most policies won’t cover that unless you have specific water backup and sump pump coverage. This endorsement is usually pretty affordable and can save you a ton of headaches and money. It covers damage from water or sewage that backs up through sewers or drains, or from a sump pump overflow. It’s a pretty straightforward add-on that many homeowners find worthwhile.

Considering Equipment Breakdown Coverage

Sometimes, the water damage isn’t from an external flood or a sewer backup, but from your own home’s systems. Think about your water heater suddenly bursting, or your washing machine hose giving out. While your policy might cover the water damage itself, it often won’t cover the cost of repairing or replacing the appliance that caused the mess. Equipment breakdown coverage can help with that. It’s designed to cover damage from sudden and accidental mechanical or electrical failures of your home’s systems and appliances. This can include things like your HVAC system, water heater, or even your refrigerator. It’s a bit more niche, but if you have older appliances or systems, it might be worth looking into.

What to Do After Experiencing Water Damage

Okay, so you’ve found water where it shouldn’t be. It’s a stressful situation, no doubt about it. But taking the right steps immediately can make a huge difference in how smoothly things go with your insurance claim and how well your home recovers. Don’t panic, just focus on these key actions.

Documenting the Damage Thoroughly

First things first, you need to create a clear record of everything that happened. This documentation is your best friend when talking to your insurance company. Start snapping photos and taking videos of the wet areas, any damaged belongings, and the overall scene. Try to capture the extent of the water intrusion. If you can, don’t move or throw away damaged items until an insurance adjuster has had a chance to see them. It’s also a good idea to start a list of everything that’s damaged, noting what it is, roughly when you got it, and what you think it’s worth. This will be super helpful later on.

Taking Steps to Prevent Further Harm

Your next priority is to stop the water from causing even more problems. If it’s safe to do so, turn off the main water supply to your home. You might also need to shut off electricity in affected areas to avoid electrical hazards. If there’s standing water, try to remove as much of it as you can. You can use buckets, wet vacuums, or even towels. Moving undamaged furniture or belongings away from wet areas is also smart. If a roof leak is the culprit, a temporary tarp might help until professionals can fix it. Keep receipts for any supplies you buy to prevent further damage, as these might be reimbursable.

Creating a Detailed Home Inventory

This might seem like a lot when you’re dealing with a mess, but having a detailed home inventory is incredibly useful. It’s not just for water damage; it’s good to have one updated regularly anyway. For water damage, specifically list out all the damaged personal items. Include details like the item’s brand, model number, age, and original cost if you remember it. This helps establish the value of your lost or damaged possessions. If you don’t have a full inventory already, start building one now for the damaged items. It’s a bit of work, but it really helps when you’re trying to get your claim settled accurately. You can find resources online to help you create a home inventory if you’re not sure where to start.

Remember, acting quickly and documenting everything meticulously are the most important steps you can take right after discovering water damage. These actions will significantly impact the success of your insurance claim and the overall recovery process for your home. Don’t hesitate to contact your insurance provider as soon as possible to let them know what’s happened and to understand the next steps in filing your claim.

After you’ve secured the area and documented the damage, reach out to your insurance company. They’ll likely assign a claims adjuster to assess the situation. Be prepared to share all the documentation you’ve gathered. It’s also wise to keep records of all your communications with the insurance company and any contractors you hire. This includes emails, phone calls, and invoices. This organized approach will make the entire process much smoother. If mold starts to become a concern due to the moisture, remember that mold cleanup might be covered if it stems from a sudden, accidental event, but not usually from gradual issues or neglect.

Wrapping It Up

So, when it comes to water damage and your homeowner’s insurance, it really boils down to the ‘why’ and ‘how’ it happened. Sudden, unexpected events like a burst pipe or a storm ripping a hole in your roof? Those are usually covered. But if the damage happened slowly over time because of poor upkeep, like a leaky faucet you never fixed or a roof that’s seen better days? That’s generally on you. It’s always a good idea to check your specific policy and maybe even chat with your insurance agent to know exactly what’s covered and what’s not. Adding things like sewer backup coverage can be a lifesaver too, especially if you live in an area prone to those issues. Being prepared and knowing your policy can save you a lot of headaches and money down the road.

Frequently Asked Questions

Does my home insurance cover water damage from a burst pipe?

Usually, yes! If a pipe suddenly bursts and causes damage, your home insurance likely covers it. But if the pipe was leaking for a long time and you didn’t fix it, that’s considered a maintenance issue and might not be covered.

Will my insurance pay to replace the appliance that leaked?

Generally, your insurance will cover the mess the appliance made, like damaged floors or walls. However, it usually won’t pay to fix or replace the appliance itself because that’s seen as wear and tear.

Is damage from flooding covered by my homeowners insurance?

Typically, no. Standard home insurance policies don’t cover damage from floods, like when rivers overflow or heavy rain causes widespread flooding. You’ll likely need a separate flood insurance policy for that.

What about water backing up from sewers or drains?

Most standard policies don’t cover this. If water or sewage backs up into your home from the sewer or drain system, you’ll probably need to buy extra coverage, often called ‘water backup and sump pump coverage,’ to be protected.

Does my insurance cover mold caused by water damage?

It depends. If mold grew because of a sudden, accidental water leak (like a burst pipe), your policy might cover it. But if the mold is from a slow leak you knew about or should have known about, it’s usually not covered.

What should I do if I find water damage in my home?

First, try to stop more water from causing damage, like turning off the water supply if possible. Then, take lots of pictures and videos of everything that’s wet or damaged. Make a list of all the ruined items. Don’t throw anything away until your insurance adjuster has seen it.